Our goal at Benchmark Commercial Lending is to provide access to commercial loans and leasing products for small businesses.

Content

Generally speaking, a company with a negative retained earnings balance would signal weakness because it indicates that the company has experienced losses in one or more previous years. However, it is more difficult to interpret a company with high retained earnings. Any item that impacts net income (or net loss) will impact the retained earnings. Such items include sales revenue, cost of goods sold (COGS), depreciation, and necessary operating expenses. If the company had not retained this money and instead taken an interest-bearing loan, the value generated would have been less due to the outgoing interest payment.

There are businesses with more complex balance sheets that include more line items and numbers. Companies, many of which publish IFRS-based financial statements, use different … While the title additional paid-in capital is the most common, there is some variation across companies. For example, The New York Times Company uses additional capital, Goodyear Tire & Rubber retained earnings uses capital surplus, and Chevron Texaco Corporation uses capital in excess of par value. The statement is important as it shows the financial health of the company and can help various stakeholders make informed decisions about the company. It also helps track how much profit has been retained over a period and can be an early indicator of potential bankruptcy.

Paying off high-interest debt also may be preferred by both management and shareholders, instead of dividend payments. Profits give a lot of room to the business owner(s) or the company management to use the surplus money earned. This profit is often paid out to shareholders, but it can also be reinvested back into the company for growth purposes. Since stock dividends are dividends given in the form of shares in place of cash, these lead to an increased number of shares outstanding for the company. That is, each shareholder now holds an additional number of shares of the company.

As mentioned earlier, retained earnings appear under the shareholder’s equity section on the liability side of the balance sheet. As an investor, you would be keen to know more about the retained earnings figure. For instance, you would be interested to know the returns company has been able to generate from the retained earnings and if reinvesting profits are attractive over other investment opportunities. For instance, a company may declare a stock dividend of 10%, as per which the company would have to issue 0.10 shares for each share held by the existing stockholders.

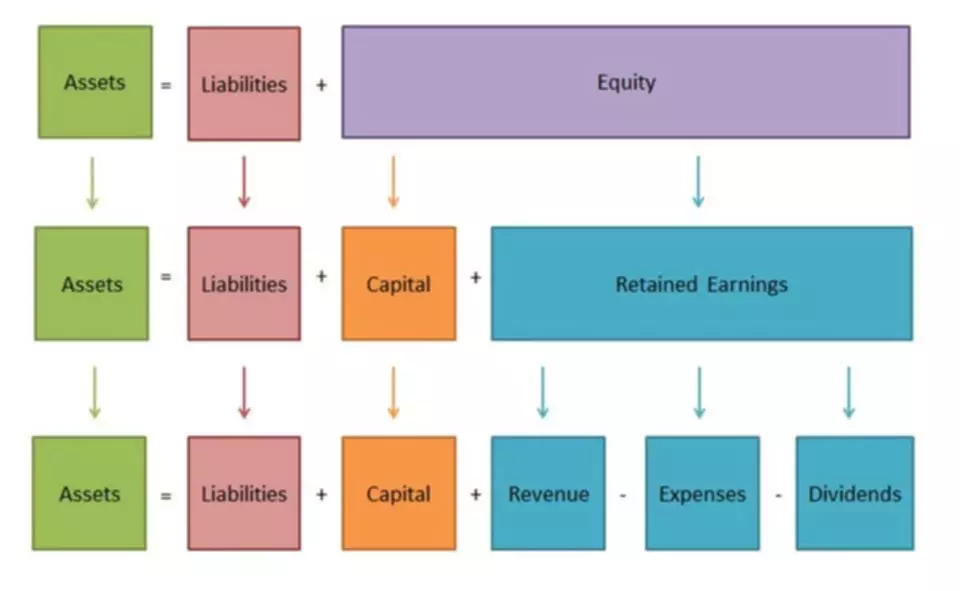

Revenue sits at the top of the income statement and is often referred to as the top-line number when describing a company’s financial performance. Retained earnings are also called earnings surplus and represent reserve money, which is available to company management for reinvesting back into the business. When expressed as a percentage of total earnings, it is also called the retention ratio and is equal to (1 – the dividend payout ratio). However, management on the other hand prefers to reinvest surplus earnings in the business.

Third, we show that book-to-market loses its predictive power in the latter subperiod because its correlation with retained earnings-to-market drops. Fourth, we obtain similar results for U.S. firms over a pre-Compustat period from 1938 through 1964. We next demonstrate the source of book-to-market’s explanatory power by entering it in a horse race against our own accumulation of past earnings over increasing windows.

This is less any dividends that have been paid out to shareholders over that time. Understanding the nuances of retained earnings helps analysts to determine if management is appropriately using its accrued profits. Additionally, it helps investors to understand if the business is capable of making regular dividend payments. Overall, Coca-Cola’s positive growth in retained earnings despite a sizeable distribution in dividends suggests that the company has a healthy income-generating business model. The growing retained earnings balance over the past few years could suggest that the company is preparing to use those funds to invest in new business projects. When lenders and investors evaluate a business, they often look beyond monthly net profit figures and focus on retained earnings.

Carbon Collective partners with financial and climate experts to ensure the accuracy of our content. The business case below, in which you will play the role of an experienced accountant mentoring an intern, will allow you to apply your knowledge about the preparation of the Statement Of Retained Earnings. Regardless of the budgeting approach your organization adopts, it requires big data to ensure accuracy, timely execution, and of course, monitoring.

In fact, both management and the investors would want to retain earnings if they are aware that the company has profitable investment opportunities. And, retaining profits would result in higher returns as compared to dividend payouts. As mentioned earlier, management knows that shareholders prefer receiving dividends.

As the company loses ownership of its liquid assets in the form of cash dividends, it reduces the company’s asset value on the balance sheet, thereby impacting RE. Finally, if the balance of retained earnings is growing over time that might not be a good thing. Intuitively you would expect a business to be growing retained earnings as it generates profits, but investors look for businesses to payout reasonable amounts in the form of cash or stock dividends. Therefore, a growing balance might indicate little cash returns for investors and might signal that management is inefficiently utilizing retained earnings. Cash dividends represent a cash outflow and are recorded as reductions in the cash account.

Since all profits and losses flow through retained earnings, any change in the income statement item would impact the net profit/net loss part of the retained earnings formula. This statement of retained earnings appears as a separate statement or it can also be included on the balance sheet or an income statement. The statement contains information regarding a company’s retained earnings, also including amounts distributed to shareholders through dividends and net income. An amount is set aside to handle certain obligations other than dividend payments to shareholders, as well as any amount directed to cover any losses. Each statement covers a specified period of time, usually a year, as noted in the statement.